As industry experts closely monitor the market, the state of the insurance industry continues to fluctuate. This can be confusing for business owners trying to forecast future insurance costs while experts try to project whether insurance premiums will rise and by how much. In this post, we examine the importance of risk management and loss control to help you prepare for increases in premiums that may come during a hard market.

What is clear is that risk management, loss control, and safety continue to be crucial to the success of any commercial insurance package, regardless of market conditions. Now is a good time to evaluate your business’s risk management plan as a whole to ensure your business can attain favorable pricing regardless of market conditions.

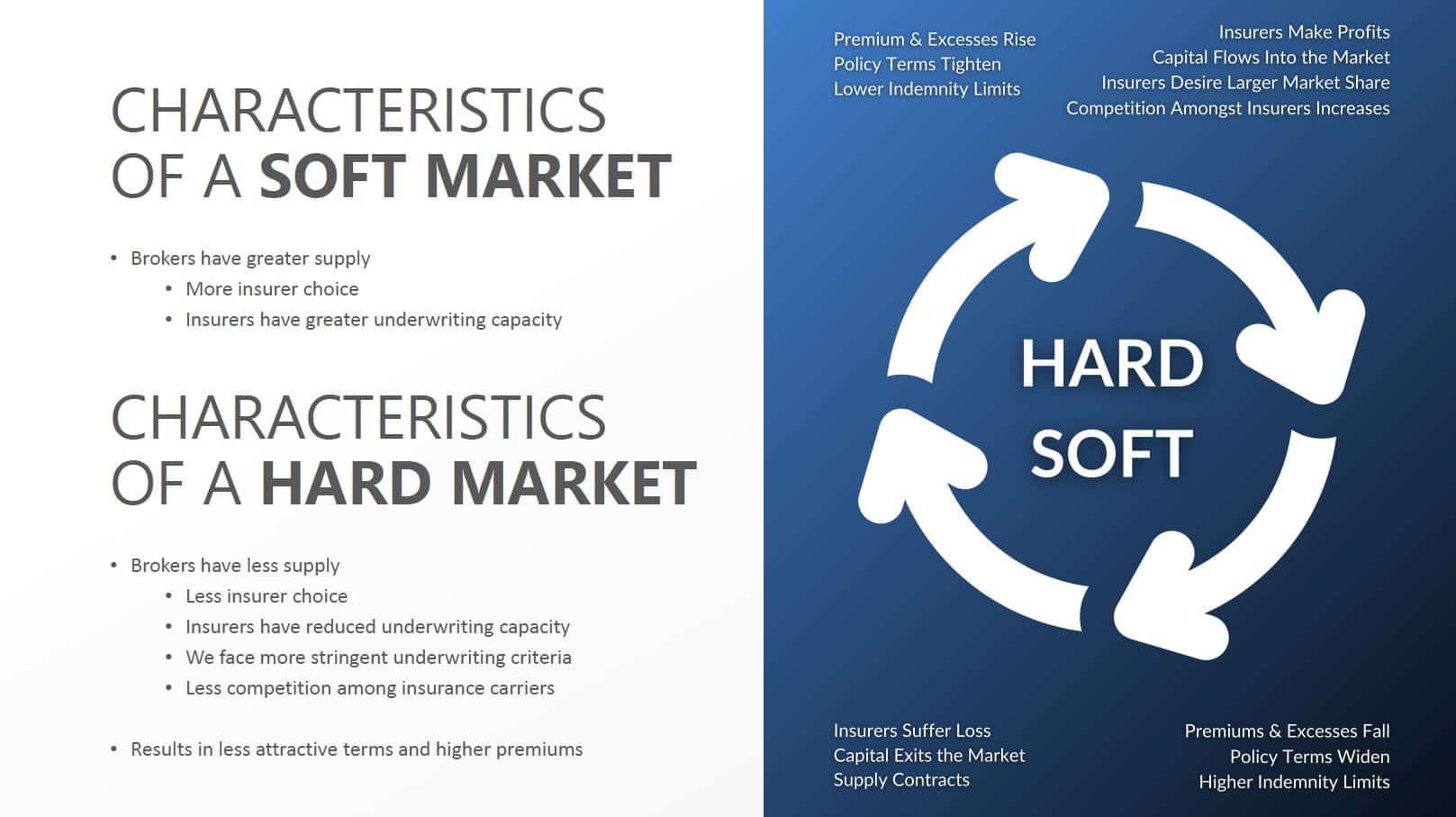

What is Driving the Hard Market?

There are a number of factors that are contributing to the tightening of restrictions. Interest rates are at an all-time low, record level underwriting losses have been recorded for several years, claims costs are on the rise, and catastrophic events all play a significant role. The frequency and severity of natural catastrophes such as fires, hurricanes, and tornadoes are costing the insurance industry billions.

Add to this list the effects of COVID-19, which are still yet to fully play out. Some experts have described the pandemic as “a slow-moving catastrophe” that basically threw gas on the fire on the hardening market.

What does a Hardening Market Means for Your Business?

During times of a soft market, like the past few years, business owners see cost reductions in their organization’s insurance premiums, even without a reduction in their risk. As a result, business owners are often unwilling to spend time and resources on loss control and risk management because they already see their insurance premiums dropping. This reduction in pricing is deceptive, setting businesses up for a shock when the market takes a turn.

It’s important to take advantage of the opportunity to get ahead of the game by proactively addressing losses and risks now. When insurance prices begin to climb, those organizations that have taken the initiative to address losses and mitigate risk will see modest increases in premiums, whereas those that simply rode the market without working to reduce risk will have a harder time placing coverage and won’t be offered as competitive of rates. As a business owner, a 15 percent increase in cost will still be unpleasant, but a 40 percent increase in addition to a reduction in coverage could end up affecting your company’s well-being in the short and long term.

Even if the market doesn’t harden soon or hardens gradually, a business with effective loss control and risk management initiatives will always pay less to secure their firm, even in the softest of markets.

Take Charge of Loss Control & Risk Management

The best approach to control losses is to prevent injury and illness, manage claims effectively and implement cost containment strategies. If you work to reduce risk and prevent loss now, the increase in your premiums later will be minimized. These are some proven ways of mitigating the impacts of a hard market:

- Anticipate the Cycles and Prepare

- Continue to assess your risk profile. Plan for future increases even in a long soft market cycle.

- Open and honest dialogue with your broker

- Not putting through small claims. Absorb higher deductibles when you can afford to do so.

- Consistent and documented risk management and safety plans formalize the process

- Slip and Fall prevention

- Fleet Management Plans

- Business Continuity and Contingency Plans

- Employee Training and Safety Training

- Let us be your trusted advisor versus just your vendor

- Tell us about operational changes before you begin.

- Allow us to review contracts so we can make sure you have the best portfolio and risk management in place to

protect your business and to allow us to ensure you are not taking on any unnecessary liabilities. - Be open to site inspections and visits.

- Make sure your Website is up to date and true to what you are doing

- When you have a claim, immediately develop a plan to mitigate future similar claims best indicator for future losses are

past ones

How Can We Help?

Simply put we are here to support you and to be your trusted advisor. We have tools to help you design the risk management plans and can help you with navigating the hard market.

Our proactive service allows us to meet with you at least twice annually and each meeting has a specific agenda and goals. These meetings help us learn more about your business. No one knows more about your business than you do, so to help us tell the best story to our insurer partners it’s our job to know, too. Where possible, let us introduce you to your underwriters or underwriting team, this way they become more invested in your business and are more likely to go to bat for you when needed the most.

Questions? Concerns? Drop us a line and we’ll be in touch.

Contact

"*" indicates required fields

Related Posts: